The Conversation

The Conversation

Governments of all stripes provide support to small businesses in the form of tax concessions, lighter-touch regulation or government grants. They’re called the “engine room” of the economy. But is small really best?

In recent research, my co-authors and I explored this question by looking at the contributions that firms of different ages and size make to the economy.

We found new and young businesses, rather than small, old businesses, are the drivers of economic growth. This matters, as the economic dynamism these young firms drive boosts productivity – the major determinant of incomes in the long run. But government policy is focused on size, which may be holding us back.

Using de-identified data from the Australian Bureau of Statistics that tracks all businesses in Australia, we analysed the economic performance of each individual business in the market sector from 2003 onward – from pubs and cafes to manufacturing.

This includes all business types and sizes, from the corner store to the major corporates. We analysed how many people they employed, their economic value-add (think of it as their contribution to the economy), and their labour productivity (how much stuff they produce for a given amount of workers and hours).

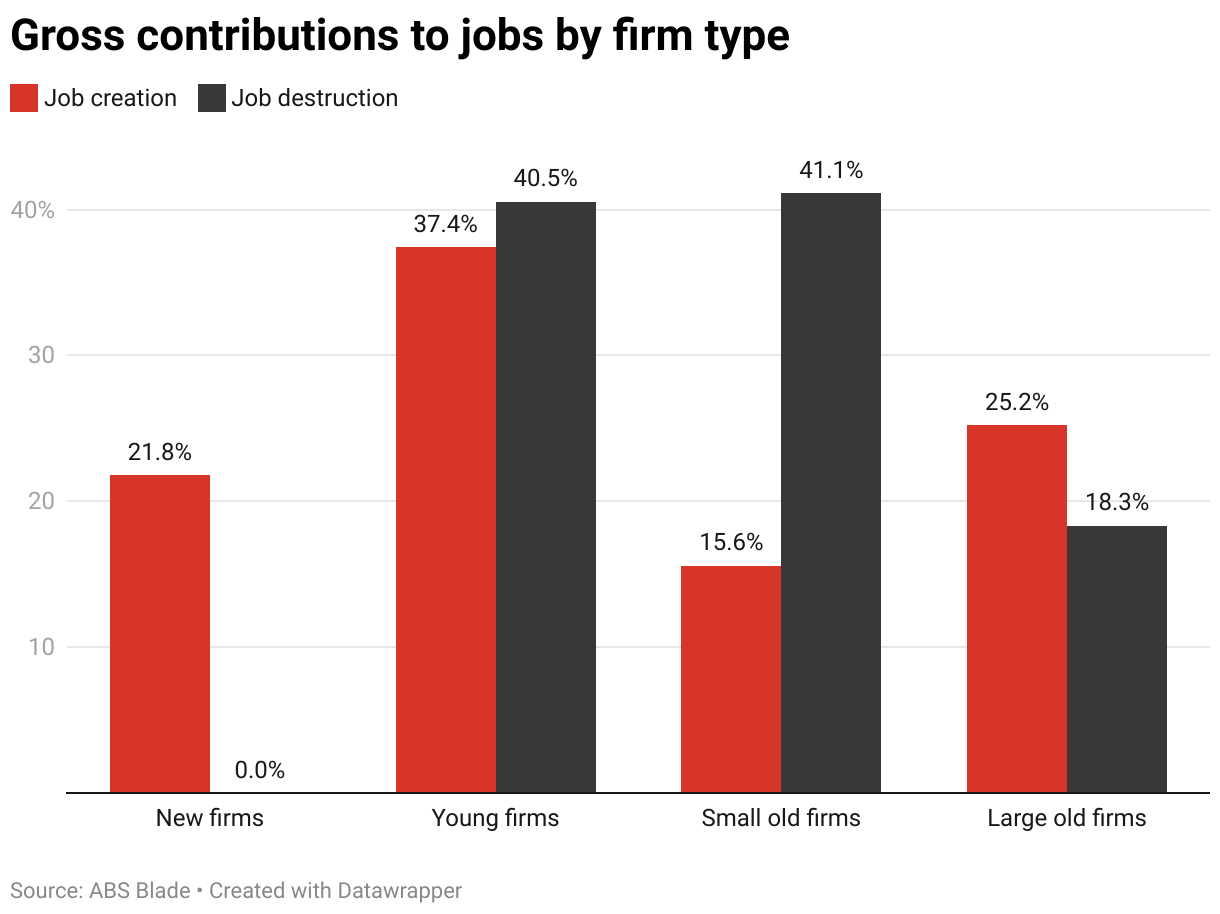

Australia has some 2.7 million small businesses, with 440,000 new businesses started in 2024-25. But our study finds it’s young firms (those aged five years or less) that punch above their weight and have an outsized positive contribution to the economy, while small, old firms (aged over five, and with fewer than 15 employees) have a net negative impact.

Engines of job creation

Our research found young businesses contribute six percentage points to overall annual headcount growth. This compares to small, old firms, which actually reduce overall annual headcount growth by 4.5 percentage points, due to these firms stagnating, shrinking and closing down.

This difference is underlined when we look separately at job creation and job destruction. Young firms contribute 59% of new jobs, while small old firms account for just 16%.

This is even more stark when comparing job losses: small old businesses account for 41% of all job destruction. Large old businesses – often the focus of announced corporate layoffs – account for 18% of job destruction.

So is young best then? As economists like to say – it depends.

We analysed the growth trajectories of young firms and found significant differences.

Of firms that survive to age five, high-performing young firms employ twice the number of workers than the average firm of the same age, and are over 40% more productive.

But the typical new business (in its first year of activity) is relatively small, employing only around two people. And it stops growing relatively quickly – on average new firms plateau after two years of operation. This highlights the vast differences in firm types among young firms.

This might not be surprising to some readers; not all new businesses are started with the goal of being the next Atlassian or Canva.

People start businesses for a range of reasons: whether you’re a lawyer who’d rather be your own boss than work for a large corporation; an IT worker who recently had a child and values control over the flexibility of your time; or a tradie who benefits from the tax implications of running your own business.

Smarter ways to support all businesses

This highlights the importance of policymakers being clear on what they’re trying to achieve when providing subsidies and support to businesses.

Our analysis suggests if the policy goal is to spur economic growth and employment, then targeting assistance to small businesses is poor policy. But this doesn’t necessarily mean we should take that assistance and give it to young firms instead.

Since a small number of high-performing young firms drive economic growth, we won’t always know which young firms these will be. Policy that subsidises young firms would potentially still be ineffective. And we know government has a chequered history with picking winners – see the more than A$30 billion provided to the car manufacturing sector.

So, what should government do?

One often overlooked and potentially counterintuitive finding from our research is the role of firm “exits” – businesses closing down or moving onto new ventures. Firms that exit are 20% less productive than the average firm in their industry five years before they close down, and their productivity declines further as they approach closure.

But the rate of business closures in Australia has been declining over time. Policies that remove impediments from orderly business closure, including supporting affected workers, would help workers and capital to be re-allocated to more productive and innovative firms.

Specific business assistance and targeting is always fraught with difficulty. Policymakers can instead focus on broader policy settings that are conducive to growth, and that apply to all firms rather than just a subset.

These efforts, such as streamlining regulation and ensuring it is fit for purpose for all businesses, would be in line with some of the principles and reform directions agreed at Treasurer Jim Chalmers’ economic reform roundtable earlier this year.

The author thanks Rachel Lee and Ewan Rankin, researchers at the e61 Institute, for their contribution to this article.

This article is republished from The Conversation, a nonprofit, independent news organization bringing you facts and trustworthy analysis to help you make sense of our complex world. It was written by: Lachlan Vass, Australian National University

Read more:

- Checking out a listing you like? Experts explain what to look out for when inspecting a first home

- The controversial GST deal with the states is under review. There are better alternatives

- New data shows the US dollar still dominates foreign exchange markets – despite Trump’s economic chaos

Lachlan Vass is affiliated with the e61 Institute.

The radio station 99.5 The Apple

The radio station 99.5 The Apple NOLA

NOLA The American Lawyer

The American Lawyer NPR

NPR Raw Story

Raw Story NBC10 Boston Entertainment

NBC10 Boston Entertainment America News

America News