The Conversation

The ConversationNew data show wages have risen by a bit more than inflation, but overall real wages are still languishing near 2011 levels.

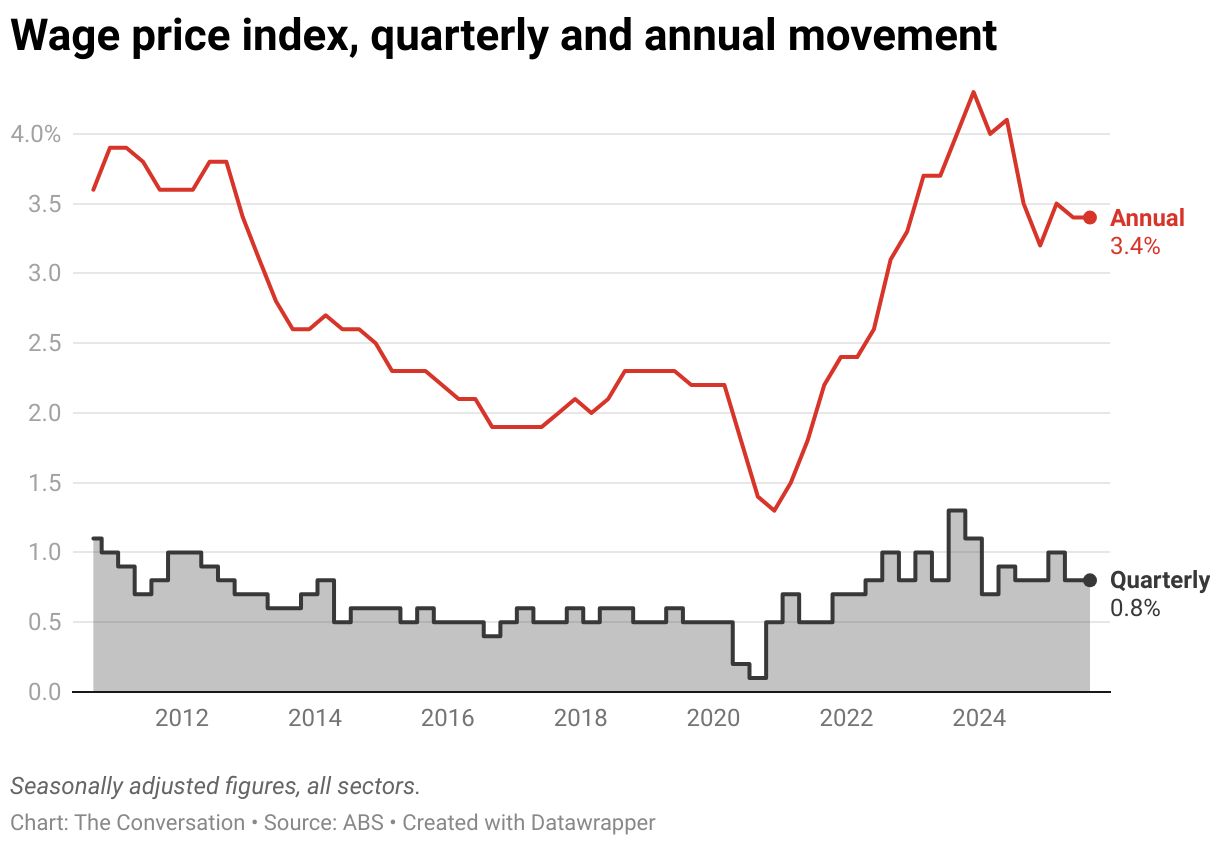

Over the year to September, wages rose 3.4% in seasonally adjusted terms. That’s according to the latest wage price index data from the Australian Bureau of Statistics (ABS), released on Wednesday.

That’s slightly more than the rate of inflation over the same period – 3.2% – meaning real wages are up by 0.2% over the year to September.

For the Reserve Bank of Australia, it means an interest rate cut in the near term remains unlikely. However, overall wages growth is nowhere near enough to make up for the huge decline in real wages over the past five years.

What is the wage price index?

The wage price index measures the average change in Australian wages and salaries every quarter. To do this, it tracks a fixed “basket” of jobs across a wide range of industries in both the public and private sector.

It doesn’t include bonuses, and it doesn’t include wage growth that comes about from people getting promoted, switching to better-paid occupations, or moving to other regions.

To illustrate, imagine a world where half of all workers were labourers and the other half were managers.

If the labourers’ hourly wage increased from $30 to $33 (a 10% increase), and the managers’ hourly wage increased from $80 to $84 (a 5% increase), the wage price index would increase by 7.5%. That is the average of 5% and 10%.

It’s an important index, but it doesn’t tell us everything. For example, it doesn’t give us the full story on wage growth, because many people grow their incomes by moving to better-paid jobs or occupations.

In our example, if an individual labourer became a manager, their wage would increase from $30 to $84 – an obvious improvement. But this change is not counted in the index.

It doesn’t tell the full story

The wage price index doesn’t give us the full story on labour costs either.

The Reserve Bank is tasked with setting interest rates to keep annual consumer inflation in a target range of 2–3%, as measured by the consumer price index.

Labour costs aren’t directly included in the consumer price index. But the Reserve Bank still keeps a close eye on wage growth, because higher wages can lead to higher costs for employers and create inflation.

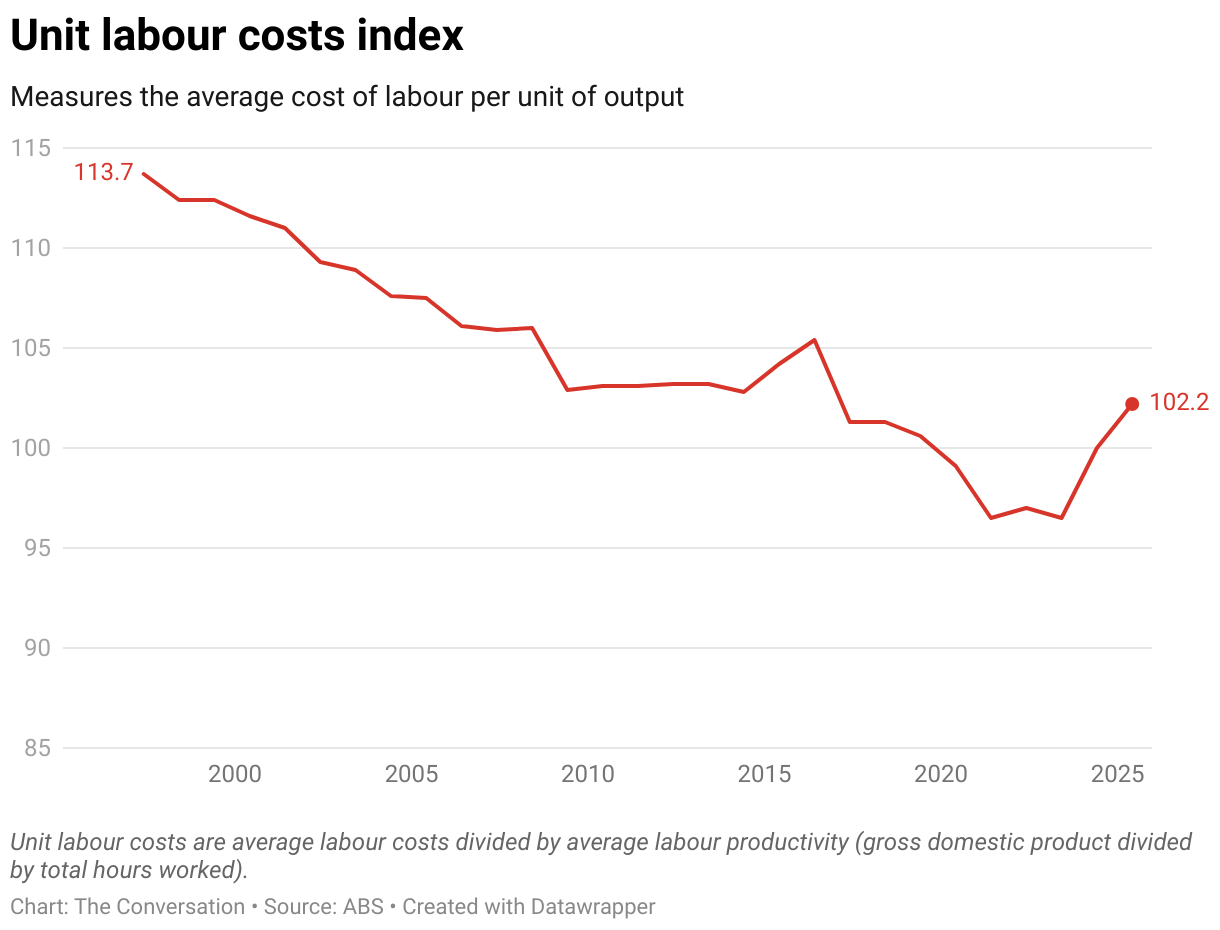

But productivity growth – the continual improvement in our ability to produce more output from the same inputs – reduces labour costs relative to the amount of income a business can generate.

The chart below shows over most of the past three decades, labour costs have fallen, because productivity growth has been stronger than wage growth. The uptick in labour costs since 2023 shows wage growth has been stronger than productivity growth for the past two years.

Have we really had a pay rise?

It feels good to get a pay rise, and governments and employers enjoy the optics.

A joint statement from Treasurer Jim Chalmers and Employment Minister Amanda Rishworth noted annual real wages have now grown for eight quarters in a row:

the longest period of consecutive annual real wage growth in almost a decade.

But how healthy are Australians’ earnings really?

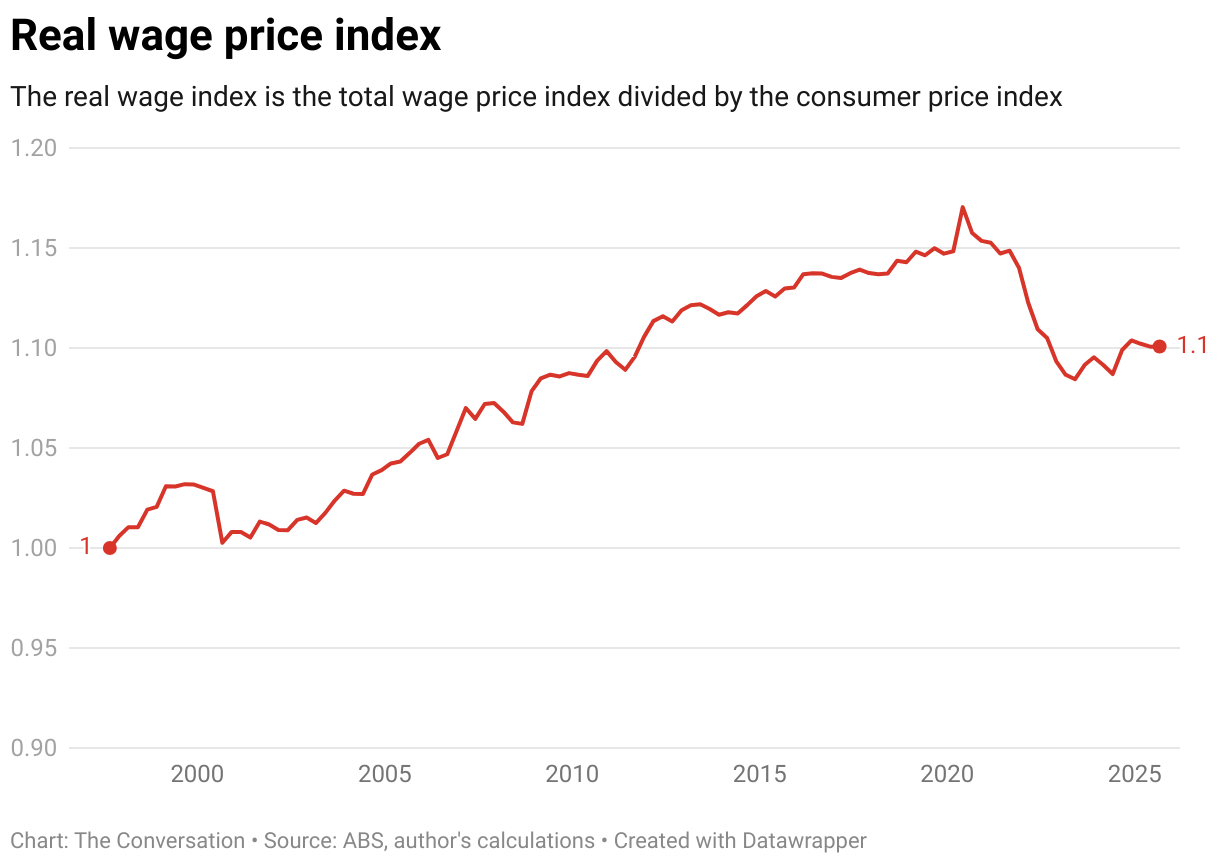

When wages grow faster than consumer prices, wage earners are able to get more bang for their buck. Until June 2020, this was the case over most of the past few decades.

But when consumer prices grow faster than wages, even if wages are rising, consumer purchasing power goes backwards. This has been the case from mid-2020 until very recently.

As the above chart shows, after accounting for inflation, Australians’ wages have roughly the same purchasing power now as they did back in 2011 – when the iPhone 4 was state-of-the-art and a Donald Trump presidency was a mere thought bubble.

The post-COVID decline in real wages is by far the largest in recent history, but it’s not the only one. In 2000, when the goods and services tax (GST) was introduced in Australia, a jump of almost 4% in the CPI led to a steep dip in real wages, which took about four years to unwind.

A lost decade

A horror stretch starting in 2020 saw an entire decade of real wage growth reversed in just three years. Today’s result consolidates a cautious return to real wages growth.

We will need to wait until the gross domestic product (GDP) figures come out next month to see whether the growth is supported by productivity gains.

While workers will welcome growth in real wages, we must be careful about what we wish for. When wage growth is not supported by productivity growth, employers will often reduce costs by laying off workers.

The seasonally adjusted unemployment rate is currently 4.3%, a low level historically, but it is trending upwards. Ongoing modest wage growth and low unemployment will help workers win back the lost decade.

This article is republished from The Conversation, a nonprofit, independent news organization bringing you facts and trustworthy analysis to help you make sense of our complex world. It was written by: Janine Dixon, Victoria University

Read more:

- Yes, migration to Australia is up. But new figures show most migrants do not become citizens

- Years in the making, the first complete monthly inflation report is almost here

- Australian businesses have actually been slow to adopt AI, survey finds

Janine Dixon does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

104FM WIKY

104FM WIKY Reuters US Economy

Reuters US Economy CBS19 News Crime

CBS19 News Crime The radio station 99.5 The Apple

The radio station 99.5 The Apple Lansing State Journal

Lansing State Journal 23ABC News Bakersfield

23ABC News Bakersfield KAWC

KAWC The Monroe News

The Monroe News Cover Media

Cover Media AlterNet

AlterNet